Skip to content

Digitalwrks

Oceana~California

Menu

Home

Comments

Category:

finance

Posted on

February 16, 2024

Dead cat bounce

Posted on

December 4, 2023

December 4, 2023

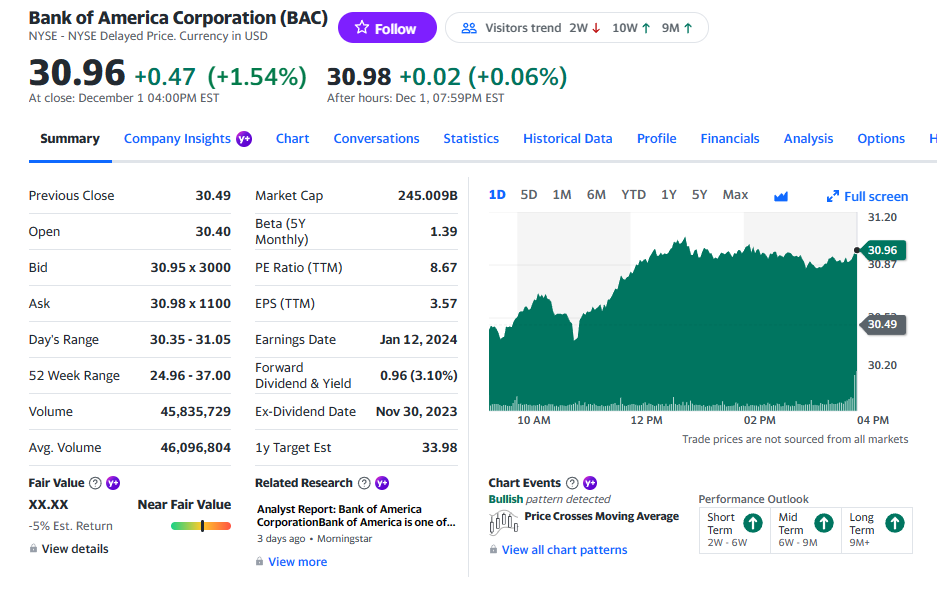

Bank of America (BAC) – At closing – 12/01